Good morning. Turned into a slightly volatile day yesterday with a firm rebuttal of the 6400 level with a drop down to 6320 again. The 1995 S&P short worked well, though in the end closed far too early. Most of that drop down was due to the IMF report on global debt. The International Monetary Fund warned officials to protect their financial systems from possible instability as the Fed prepares to raise interest rates, saying shocks or policy missteps risk derailing the global economy and triggering equity market selloffs. This followed a separate report in which the IMF cut its outlook for global growth this year to 3.1 percent from a July forecast of 3.3 percent.

US & Asia Overnight from Bloomberg

Asian stocks rose for a seventh day, following U.S. shares higher, with Chinese markets set to open after a week-long holiday that saw a global equity rally.

The MSCI Asia Pacific Index gained 0.2 percent to 131.95 as of 9:00 a.m. in Tokyo, heading for an almost seven-week high. Chinese markets, which were at the epicenter of August’s global turmoil, will trade for the first time since Sept. 30. The Hang Seng China Enterprises Index, a gauge of mainland shares traded in Hong Kong, has jumped 11 percent since then, with stocks around the world posting their longest rally since April. Investors are betting the Federal Reserve will keep interest rates near zero for longer, spurring demand for assets that benefit from an environment where borrowing is cheap.

“There’s been a little bit of a relief rally amid speculation the Fed will delay raising rates,” said Tim Schroeders, a portfolio manager who helps oversee about $1 billion in equities at Pengana Capital Ltd. in Melbourne. “I wouldn’t hold my breath that the rally can continue until the end of the year. Ultimately investors will come around and start to realize that the rate increase is being delayed because the economy isn’t that strong.”

Odds of a Fed liftoff in 2015 have fallen below 50 percent after a weaker-than-expected U.S. jobs report last week reduced the case for the Fed to raise interest rates this year.

Japan’s Topix index lost 0.1 percent. South Korea’s Kospi index added 0.5 percent. Australia’s S&P/ASX 200 Index rose 0.9 percent. New Zealand’s S&P/NZX 50 Index was little changed. Markets in China and Hong Kong have yet to open.

H-share Rally

Futures on the H-share gauge slid 0.8 percent in most recent trading after the underlying measure surged 4.7 percent on Wednesday. Contracts on the FTSE China A50 gauge of the mainland’s largest stocks slipped 0.7 percent. Shanghai shares were hovering near their 2015 low before the holidays as mounting signs of a slowdown in China and its potential to spread throughout the world economy fueled a selloff last quarter.

Futures on the Standard & Poor’s 500 Index slipped 0.1 percent on Thursday. The underlying equity measure advanced 0.8 percent on Wednesday as biotechnology companies rebounded and energy shares extended their longest rally since December 2013. The Stoxx Europe 600 Index rose for a fourth day, adding 0.1 percent. [Bloomberg]

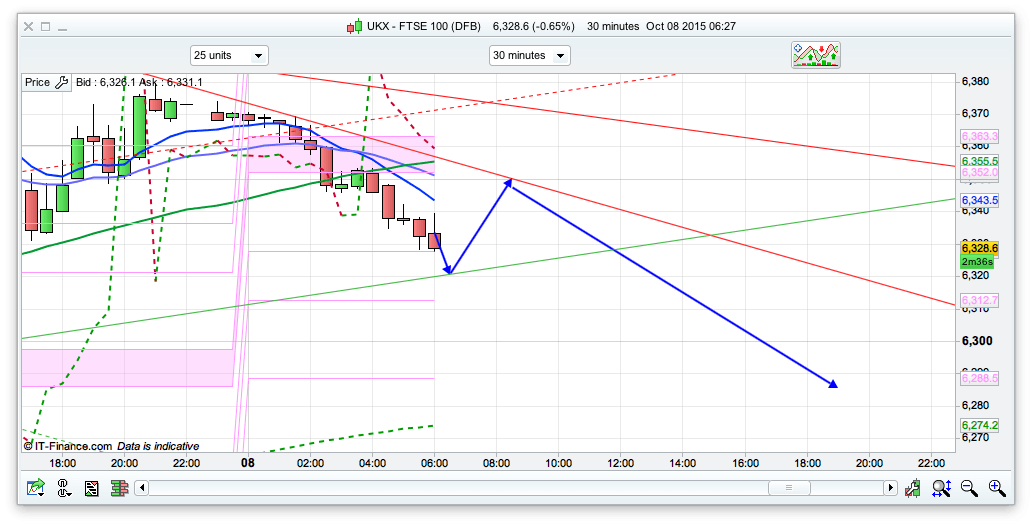

FTSE Outlook

The bulls were quite resilient yesterday but I am still feeling bearish, maybe was just 24 hours early but I think we will see some declines today and tomorrow. My 2 hour chart has resistance at 6400, thought he 30min is looking better for initial downside, with the 6350 level being the 25ema and a decent entry. With the pivot here too at 6352 I fell that this is a good level to short from and “shorting the rallies” is a good plan for the next 48 hours. We have China back from their 5 day break today , and the ASX has had a weak session dropping 0.7%. I think the FTSE will have a negative day today as well.