Good morning. It was a day of profit taking after recent rises kicked off in part by poor company results and a slightly more hawkish outcome of the US interest meeting than expected. Weaker than expected US data also kept markets down in the afternoon. Overnight the Bank of Japan have left monetary policy unchanged and refrained from adding further stimulus, waiting to see what the Fed does next I expect. We had a decent hold of the lower support area yesterday – 6370 where we had the 10 day Bianca channel, though the bulls made handwork of pulling away from it, and it did look like it was going to break for a while. However, once the market closed the US dragged the FTSE up, and back above 6400 as I am writing this, which is now a support level.

US & Asia Overnight from Bloomberg

Asian stocks stayed on track for their biggest monthly gain in five years as investors awaited a Bank of Japan decision on monetary policy.

The MSCI Asia Pacific Index was little changed at 133.85 as of 9:05 a.m. in Tokyo, with Australian banks dragging on the gauge while Samsung Electronics Co. jumped. The measure is up 8.1 percent in October, led by a rebound in energy shares. Economists are split on whether the BOJ will add to its unprecedented easing on Friday.

“The key question today is the BOJ and whether they will follow the European Central Bank lead in signaling or even delivering further policy stimulus,” Sharon Zollner, a senior economist at ANZ Bank New Zealand Ltd. in Auckland, said in a client note. “Further stimulus, or a promise thereof, would alter market dynamics, offsetting the Fed normalization pulse.”

Japan’s Topix index slipped 0.1 percent. Further easing would pit Japan and the European Central Bank, which indicated last week it would increase bond purchases should the economy require it, against the Fed, which signaled Wednesday that it’s prepared to raise borrowing costs as soon as December. It’s also a busy day for earnings reports in Japan, with more than 300 companies scheduled to publish figures.

South Korea’s Kospi index was little changed. Australia’s S&P/ASX 200 Index fell 0.8 percent and New Zealand’s NZX 50 Index lost 0.5 percent. Markets in China and Hong Kong have yet to start trading.

One-Child Policy

Chinese stocks posted their biggest three-day loss in a month in Hong Kong as earnings at some of the nation’s largest companies missed estimates, with the Hang Seng China Enterprises Index sliding 1.1 percent on Thursday.

At the end of the Communist Party’s four-day plenum, China abandoned the one-child policy that has shaped society since the late-1970s as the ruling Communist Party tries to boost a shrinking workforce and manage the country’s transition to an era of slower economic growth. The country needs annual growth of at least 6.53 percent in the next five years to meet the government’s goal of establishing a “moderately prosperous society,” Premier Li Keqiang said in an Oct. 23 speech to Communist Party members, according to people familiar with the matter who asked not to be named as the remarks weren’t public.

E-mini futures on the Standard & Poor’s 500 Index climbed 0.1 percent on Friday. The underlying gauge slipped less than 0.1 percent on Thursday. Odds the Federal Reserve will increase rates at their next meeting jumped to 50 percent from about 34 percent a week ago, based on futures prices, after officials signaled they’re prepared to tighten policy amid the waning impact of global market turbulence.

“The market continues to trade on every Fed utterance,” Michael Cuggino, the San Francisco-based president and portfolio manager at Permanent Portfolio Family of Funds Inc., said on Bloomberg TV. “By trying to be transparent and by trying to keep everybody informed, they’ve actually spoken so much through so many different voices that they’ve created uncertainty.” [Bloomberg]

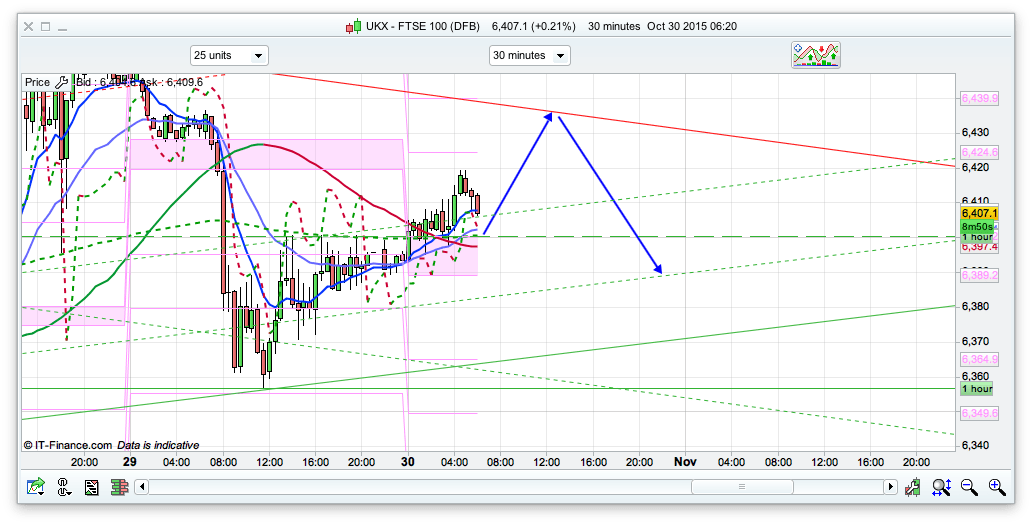

FTSE Outlook

Initially the 6400 level looks to be fairly decent support so the bulls might be keen to built not he overnight rises for a push towards the top of the 30 minute channel at 6435ish, before more downside going into the weekend. If the bulls break this level the the top of the 10 day Bianca at 6477 is likely be hit, which would be just over 100 up from the touch of the bottom of 10 day channel yesterday. Thus a decent rise and area that could see a turn back down. On the daily chart we also have the 200ema at 6513, and the top of the Raffs at around the 6530 area though I am not expecting them to be seen today. 6435 looks fairly key now as resistance also worth a short off this area, and its also the area that we dropped off from yesterday with that early bearishness. If the bears break 6400 initially however, then a drop down to the 6365 area looks likely, where upon we would have a second test of the bottom of the 10 day channel. Whilst on the face of it, it appears bullish, I wouldn’t be surprised if we start another leg down shortly, before the end of the year sees another rise (thinking a year end close around the 6600 level). Its the last trading day of the month after some decent rises during October so we may well see some profit taking towards the end of the session.