Good morning I hope you had a good weekend. Start of a new month and the penultimate one for the year end. October ended on a slightly bearish note, with the FTSE dropping off from its recent highs after nearly challenging for 6500. The break below 6345 on Friday makes things look a bit bearish on the daily chart, but we do have the bottom of the 20 day Bianca at 6330, pretty much where we are as I write this. The Dow has certainly dropped off from the 17750 area now, though it did of course pop a little bit higher than that in what looked to be a bit of a fake move (RSI, Stochs and MACD were all bearish, so bearish divergence while it rose above 17750). HSBC announced a $6.1bn profit for the third quarter, which should help buoy up the financials this morning on the FTSE. The ASX200 (Australia) was bearish today which could well follow through to the FTSE (or maybe just a rugby reaction?!)

US & Asia Overnight from Bloomberg

Asian stocks dropped, after their best month since May 2009, as industrial companies led losses following data signaling a contraction in Chinese manufacturing.

The MSCI Asia Pacific Index fell 0.5 percent to 133.77 as of 9:01 a.m. in Tokyo. The measure rallied 8.6 percent in October as China cut interest rates and the European Central Bank hinted at potential extra stimulus, while U.S. and Japanese policy makers kept their monetary policies accommodative. China’s first key indicator this quarter, an official factory gauge, missed analysts’ estimates, signaling that the manufacturing sector has yet to bottom out as global demand falters and deflationary pressures deepen.

“I’m struggling to see catalysts to encourage the market to take this rally to the next level,” said Tony Farnham, a strategist at Patersons Securities Ltd. in Sydney. “China’s PMI numbers were underwhelming. Manufacturing will probably remain weak as China tries to rebalance its economy away from manufacturing and into services.”

The purchasing managers’ index was unchanged at 49.8 in October, the National Bureau of Statistics said Sunday, compared with the median estimate of 50 in a Bloomberg survey. The non-manufacturing PMI, a barometer of services and construction, fell to 53.1 from 53.4 in September, the weakest since December 2008. Final numbers for the private Caixin China factory PMI are due Monday, with economists surveyed by Bloomberg projecting a reading of 47.6.

Japan’s Topix index slid 1.4 percent after the yen gained 0.4 percent against the dollar on Friday. While the BOJ refrained from easing monetary policy last week, the Nikkei newspaper reported that the government may introduce additional budget measures if third-quarter gross domestic product, which will be announced on Nov. 16, shows the economy needs aid.

South Korea’s Kospi index added 0.2 percent. Australia’s S&P/ASX 200 Index lost 0.6 percent and New Zealand’s NZX 50 Index was little changed. Markets in China and Hong Kong have yet to start trading.

Futures on the China A50 index fell 0.2 percent in most recent trading, while contracts on the Hang Seng China Enterprises Index lost 0.4 percent. The Shanghai Composite Index posted its biggest monthly advance since April as the Chinese government took measures to end a $5 trillion rout and policy makers introduced stimulus to boost economic growth.

E-mini futures on the Standard & Poor’s 500 Index dropped 0.2 percent. The underlying gauge of U.S. equities slipped 0.5 percent on Friday as weaker-than-estimated quarterly results weighed on financial and consumer staples shares.

European Central Bank President Mario Draghi said that it’s still an “open question” whether stimulus needs to be increased to bolster the economy. [Bloomberg]

FTSE Outlook

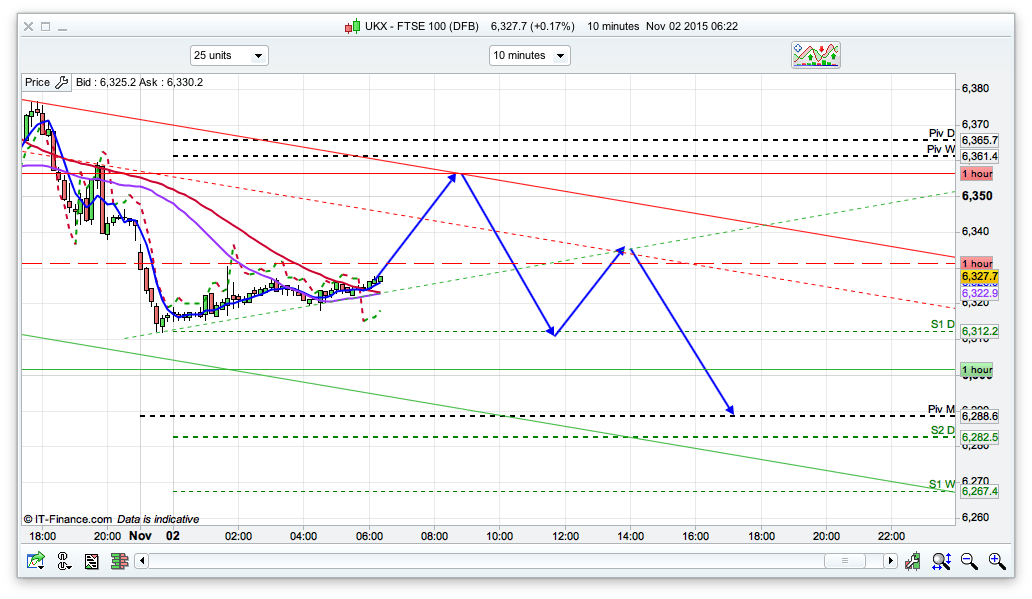

As its the start of the new month I expect that we will get an initial rise with the influx of new cash, however there is some quite strong resistance levels at around the 6360 area so we may well then mimic the Australians today and see some weakness creep in. The 2 hour chart is looking a bit bearish at the moment, with resistance at the 6375 level, and with the daily pivot at 6365 this could be the area that the bulls run out of steam today. The 200ema on 30min is currently at 6380, so that will also be resistance at that sort of level as well. Poor data out of China (PMI figures showed factory production declining again) is also likely weigh on investors mind again, and we all remember the reaction last time everyone though China was slowing down. So for today, it looks bearish really, and shorting the rallies after an initial bit of a rise looks is my plan.