Good morning I hope you had a good weekend. NFP on Friday exceeded expectations by quite a margin, which in turn weighed on the markets as focus moved to the real possibility of rate rises sooner (in the US certainly). We had Mark Carney in the UK saying that the BoE wouldn’t be raising rates for a while yet (2017 was implied) – wouldn’t surprise me if thats just a red herring though. So, despite the spectre of rate rises, the FTSE has fought back from the 6330 low set after the news broke and has held onto its modest rise as well.

US & Asia Overnight from Bloomberg

Asian stocks outside Japan dropped as a strong U.S. payrolls report bolstered the case for higher interest rates this year and data showed Chinese exports fell for a fourth month. Japanese shares gained after the yen weakened.

The MSCI Asia Pacific Excluding Japan Index lost 0.7 percent to 420.57 as of 9:52 a.m. in Tokyo. Japan’s Topix index climbed 1.4 percent after the yen slid against the dollar on Friday, improving earnings prospects for the nation’s exporters. Odds on the Fed increasing its benchmark rate in December jumped to 68 percent after data showed a 271,000 gain in U.S. payrolls in October, the biggest this year and exceeding all estimates in a Bloomberg survey of economists.

“Strong U.S. jobs data for October supports the case for a December Fed rate hike,” said Shane Oliver, Sydney-based strategist at AMP Capital Investors Ltd., which oversees about A$156 billion ($110 billion). “The Fed is unlikely to do anything to threaten global growth and this in turn should help see the global economic recovery continue. As such, share markets are likely back in a broad rising trend.”

The jobless rate fell to a seven-year low of 5 percent and average hourly earnings over the past 12 months climbed by the most since 2009. The median forecast called for a 185,000 advance in payrolls. Estimates of 75 economists in the Bloomberg survey ranged from gains of 75,000 to 250,000. Revisions to prior reports added a total of 12,000 jobs to the August and September readings.

South Korea’s Kospi index lost 0.6 percent. New Zealand’s S&P NZX 50 Index gained 0.1 percent. Australia’s S&P/ASX 200 Index fell 1.4 percent. Markets in China and Hong Kong have yet to start trading.

China Trade

Futures on the FTSE China A50 Index of the nation’s biggest companies dropped 0.9 percent in most recent trading, while contracts on the Hang Seng China Enterprises Index of mainland shares listed in Hong Kong fell 0.6 percent.

Overseas shipments dropped 6.9 percent in October in dollar terms, the customs administration said, a bigger decline than estimated by all 31 economists in a Bloomberg survey. Weaker demand for coal, iron and other commodities from declining heavy industries helped push imports down 18.8 percent, leaving a record trade surplus of $61.6 billion.

China will lift a five-month freeze on initial public offerings by the end of the year, removing one of its key measures of support for the stock market as equities recover from a $5 trillion rout. New share offerings will restart after improvements to the listing system, Deng Ge, a China Securities Regulatory Commission spokesman, said at a briefing in Beijing.

E-mini futures on the Standard & Poor’s 500 Index slid 0.1 percent on Monday. The underlying U.S. equity gauge slipped less than 0.1 percent on Friday. [Bloomberg]

FTSE Outlook

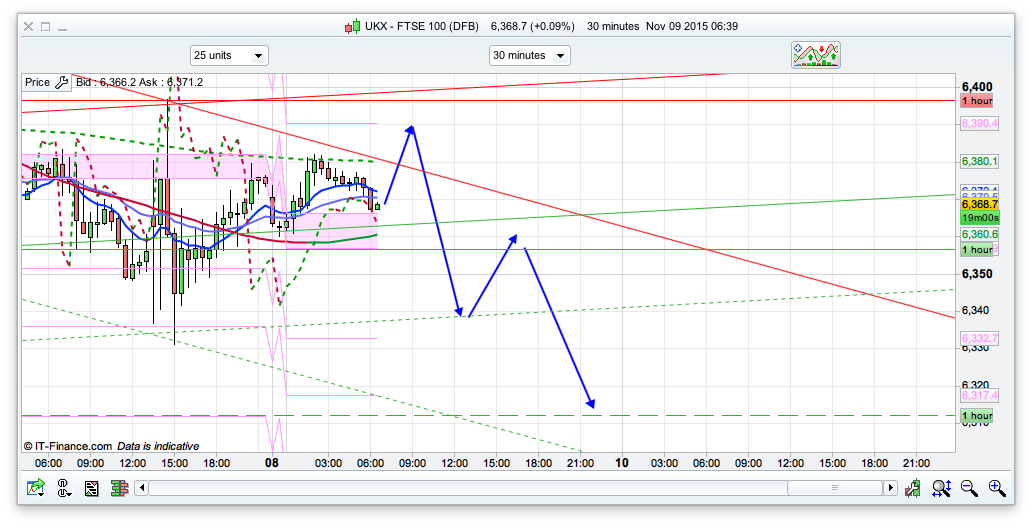

All fairly quiet on the news front over the weekend with it being remembrance Sunday. Given Fridays reaction to the NFP news I think the bulls have a bit of a job to push on to new highs at the moment, especially as the S&P has dipped back from its all time highs that it reached last week. The Bianca 10 day Channel is heading downwards, so I am still thinking that shorting the rallies is a good stance to have at the moment. We are sitting on the daily pivot as I write this, at 6367 so may see an initial rise this morning from this area, most likely to test the 6380 area, or maybe a little bit more as there is a declining 10 min channel with resistance at 6387 as well. The bulls will be hoping to break this level to reach the 6412 area where there is that 10 day channel top, but 6380ish looks key to watch first thing. If the bears hold that then a decline down to supports at 6355, 6340, and 6312 is on the cards. Considering the recent bullish vibes in the US, the FTSE is a long way from its recent 6700 level and also the 7100 tested at the beginning of the year.