Good morning. I said yesterday that it looked negative but never expected the “suckers rally” to get back to the 6450 followed by a fall to 6200! Was a bit annoying as I shorted the FTSE, Dax and S&P a bit too early with my orders on yesterdays email. At least Gold played ball for once with its rise from 1051. The 3 month FTSE high was quickly killed off by a European Central Bank policy update which fell well short of high hopes for extreme dovishness. While ECB President Mario Draghi added to stimulus, investors anticipated deeper cuts to the deposit rate and an increase in the amount of month bond purchases. This was the main news of the day in Europe and drove shares sharply lower throughout the afternoon. In the U.S., Federal Reserve Chair Janet Yellen reiterated her stance that the economy is strong enough to withstand tightening. She delivered a cautiously upbeat outlook for the economy, signaling for a second day that the conditions for higher interest rates have been met. This further fuelled the sell off! In after hours trading the FT100 has bounced off 6200, so maybe this is the bottom. The risers were constrained to a handful of special situations and fallers covered just about everything else with no standout sector.

US & Asia Overnight from Bloomberg

Emerging-market stocks declined for a third day and currencies of Asian developing nations strengthened after the European Central Bank’s stimulus disappointed some investors who had expected it to offset a likely increase in U.S. interest rates.

All 10 industry groups in the MSCI Emerging Markets Index fell, with technology companies including Samsung Electronics Co. leading the drop. A gauge of developing-nation currencies was steady after rising the most in seven weeks on Thursday, when the ECB cut its deposit rate by less than forecast and refrained from enlarging its bond-buying program. South Korea’s won headed for its first gain versus the dollar in seven days and the offshore yuan jumped as data showing slower growth in U.S. service industries supported the case for gradual monetary tightening by the Federal Reserve.

A divergence in policy outlooks in the U.S. and Europe sent the measure of emerging stocks to a record low earlier this year, and buoyed the dollar as the Fed draws closer to raising its near-zero interest rates that have supported demand for riskier assets. Fed Chair Janet Yellen signaled in her testimony before Congress Thursday that the world’s largest economy is almost ready for higher borrowing costs. While Asian currencieshave fallen versus the greenback in 2015, most have strengthened against the euro, giving European manufacturers of cars and electronics a competitive advantage.

“The ECB’s monetary easing has disappointed most investors,” said Warut Siwasariyanon, the head of research at Asia Wealth Securities Co. in Bangkok. “Yellen’s comments support the case for outflows from emerging markets, and equities should face further pressure from higher U.S. rates and the dollar’s overall strength.”

Stocks

The MSCI Emerging Markets Index dropped 0.5 percent Friday and 1.4 percent since Nov. 27 as of 1:51 p.m. in Hong Kong, poised for its second weekly loss. Chinese social media and gaming company Tencent Holdings Ltd. fell 2.9 percent, the biggest drag on the gauge, while Samsung Electronics retreated 1.5 percent. The measure has dropped 15 percent this year and traded at 12 times projected 12-month earnings. The MSCI World Index of developed nations has fallen 1.8 percent and is valued at a multiple of 17.

China’s stocks fell for the first time in five days, with the Shanghai Composite Index retreating 0.9 percent as financial companies declined as initial public offerings resumed after a five-month freeze. The gauge advanced 4.3 percent this week through Thursday on speculation the central bank will extend monetary easing as the government tackles the sharpest economic slowdown in a quarter of a century.

Ten Chinese companies began IPO subscriptions for IPOs this week, the first of 28 offerings this month that could tie up 3.4 trillion yuan, according to estimates compiled by Bloomberg. China Securities Regulatory Commission has approved a second batch of 10 IPOs, according to a statement on its official microblog. The Hang Seng China Enterprises Index of mainland stocks listed in Hong Kong dropped 1.2 percent.

The Philippine Stock Exchange Index fell 1.1 percent, while the South Korea’s Kospi index lost 0.5 percent. Equities gauge in Indonesia, India, Thailand and Taiwan fell at least 0.6 percent.

Bonds

Most Asian government bonds fell following a selloff in U.S. and European debt sparked by the ECB’s announcement. The yield on South Korea’s 10-year sovereign notes climbed six basis points, the most in almost four weeks, to 2.32 percent, while the three-year yield rose three basis point to 1.79 percent. Thailand’s 2025 bonds also fell, with the yield adding three basis points, to 2.70 percent. India’s 10-year yields rose two basis points to 7.73 percent before an auction of 150 billion rupees ($2.2 billion) of government securities. [Bloomberg]

FTSE Outlook and Prediction

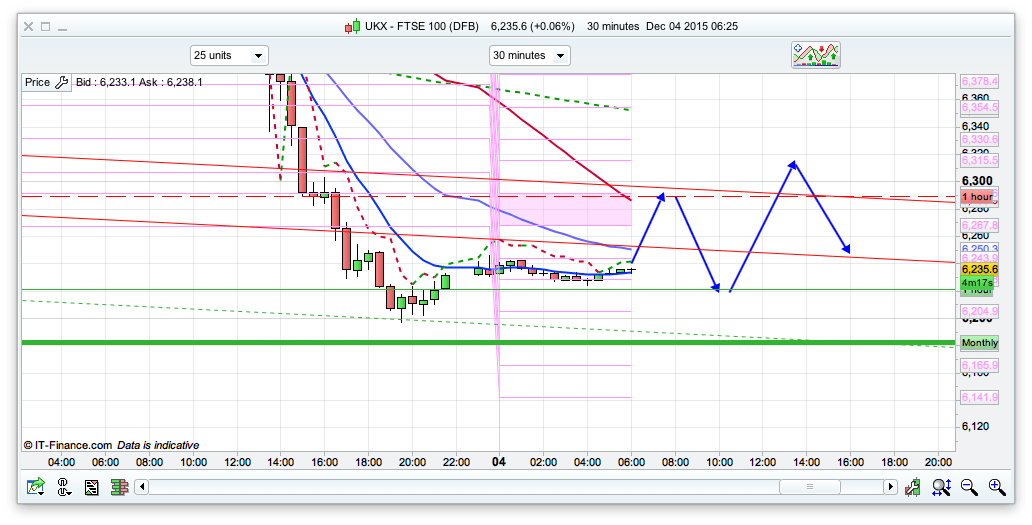

Quite a sell off yesterday and we have US jobs news out today at 13:30 with a forecast of 5% again for the unemployment rate and 200k for the change in NFP. Of course this data will be getting interpreted by the markets to see if Yellen can follow through on her talk yesterday about the economy being strong enough to warrant rate rises. There are quite a few support and resistance levels in play today after just a big swing yesterday, with PRT calculating the range at the moment between 6182 and 6444 – so worth a long at 6182 if seen. I think however that the 6215 might hold initially for a rise towards 6300, mainly as we are testing the bottom of the Raff channels on both the Dax and FTSE at 10700 and 6200 respectively. Initially the bulls need to break 6250 on the 30min chart as we have 25ema resistance here, and it would be the first touch since the cross to bear yesterday at the 6411 area. So, NFP Friday after a massive sell off so likely to be jittery, however the overnight low of 6200 has held and there is the possibility for a rise back to the 6300 level.