Good morning. The FT100 rose initially on the back of weakness in the pound, as data showed UK earnings grew at the slowest pace since the start of the year. Later in the day all eyes were on the FED which kept many shorters out of the market and so the index gradually moved its way up to the close. At 7pm(UK) the FED announced the expected 0.25% guidance increase and also provided guidance on the next year with probable 0.25% increases each quarter. This was in line with expectations and after an initial spike to 6133 on IG the FT100 fell back to a more stable 6080 at around 7:45pm and then started to move higher again. Slightly ironically the trade that did well yesterday was the 2060 S&P short!

How this will affect today’s trading is difficult to say, however with more certainty about the FED guidance it should provide positive support. A few days ago the 6400-6500 level looked a bit of a “pipe dream” but after recent rises it should not be ruled out by the end of 2015!

US & Asia Overnight from Bloomberg

Asian stocks rose, with the regional benchmark index heading toward its biggest two-day gain since early October, after the Federal Reserve raised U.S. interest rates for the first time in almost a decade and signaled a gradual pace for future increases.

The MSCI Asia Pacific Index climbed 0.9 percent to 130.73 as of 9:09 a.m. in Tokyo, heading for a two day advance of 3.2 percent, as banks and health-care shares led gains. The Standard & Poor’s 500 Index capped its biggest three-day rally since Oct. 5 as Fed Chair Janet Yellen expressed confidence the world’s largest economy is resilient enough to withstand future increases in borrowing costs.

“There’s a sense of relief that they finally raised rates,” Chris Green, an Auckland-based strategist at First NZ Capital Group Ltd., a brokerage and wealth management firm, said by phone. “This is a net positive in terms of market sentiment. It’s removed the point of liftoff from the discussion, we’re over that hurdle. Now the question is: how gradual is that normalization profile and where do the risks lie.”

In a move that was widely telegraphed, the Federal Open Market Committee unanimously voted to set the new target range for the federal funds rate at 0.25 percent to 0.5 percent, up from zero to 0.25 percent. Policy makers separately forecast an appropriate rate of 1.375 percent at the end of 2016, the same as September, implying four quarter-point increases in the target range next year, based on the median number from 17 officials.

Rate Divergence

The U.S. rate increase solidifies the Fed’s divergence from other major central banks, with policy makers in Europe and Japan still emphasizing measures to support growth. The Bank of Japan starts Thursday a two-day meeting where policy makers are expected to maintain record stimulus.

Japan’s Topix index rallied 1.8 percent as the yen weakened, sending the gauge toward a two-day advance of 4.4 percent. Australia’s S&P/ASX 200 Index jumped 1.7 percent, while New Zealand’s S&P/NZX 50 Index increased 0.2 percent. South Korea’s Kospi added 0.9 percent. Markets in China and Hong Kong have yet to start trading.

Mainland Chinese stocks in Hong Kong rallied Wednesday by the most in a month after valuations on the gauge fell to their lowest level relative to global peers in 12 years. The Hang Seng China Enterprises Index climbed 2.1 percent, the steepest advance since Nov. 4, as PetroChina Co. and China Petroleum & Chemical Corp. surged after the government signaled it won’t cut fuel prices. The Shanghai Composite Index gained 0.2 percent.

E-mini futures on the S&P 500 Index slipped 0.1 percent after the underlying measure climbed 1.5 percent Wednesday on the Fed’s rate announcement.

The central bank’s action ends an era of unprecedented monetary stimulus that pushed U.S. stocks higher by more than 200 percent and added $15 trillion in value during the 6 1/2 year bull market. Investors will now find out how much stocks are worth in the absence of Fed support, and how high borrowing costs will be without the central bank stoking growth as aggressively. [Bloomberg]

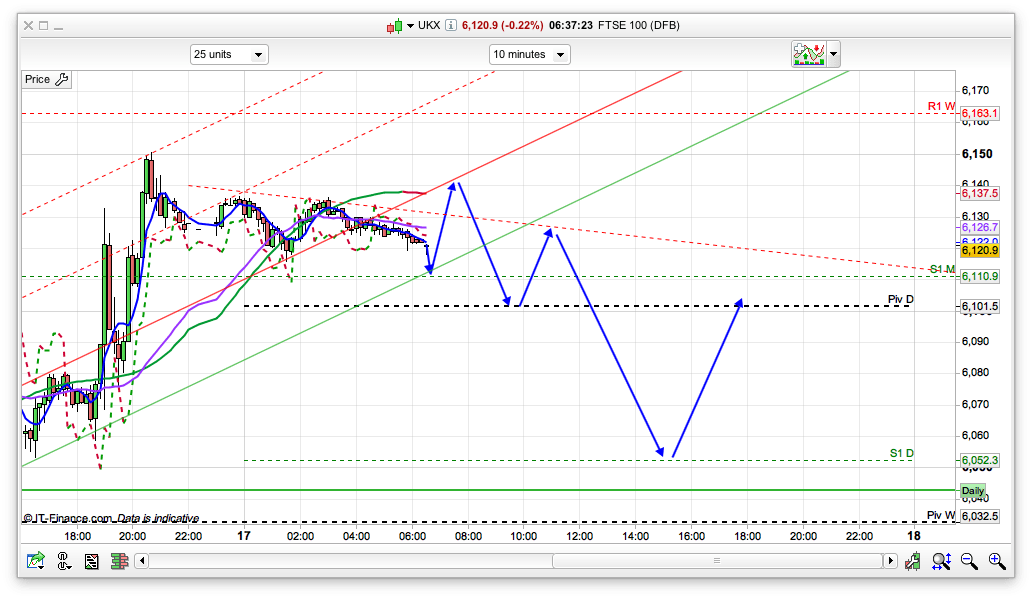

FTSE Outlook and Prediction

It could well be one of those funny days today, however the rate rise was largely as expected and thus we might well just get a bit of business as usual today. The daily pivot is support at 6101 to start with today, with the 6140 showing as initial resistance on the 10minute chart, so we may well get a dip back to start with today, down to the pivot before a bounce. However, the 30min chart might go bearish at that point so I expect we might well see some profits being banked from the recent longs. Generally it would appear that the Santa Rally has started on the 16th December once again. If the 30min does go bearish at that point then a dip down to 6050 looks possible today to consolidate some of the gains. Will we reach 6500 or more before the year end? Seems a bit of a big ask but you never know. We are just testing the top of the Raff channels at 6150 today with 6200 and 6280 as resistance levels above this on the daily chart, so the bulls have certainly got a job on their hands. Just moving back to todays possible route, there is a chance of a dip down to 6050, which looks like a good place for a long. The bulls will need to break 6150 on the upside to enable a push higher, but I think might be a bit of a day of the market catching its breath, albeit with a possible 100 point range!