Support 6135 6133 6117 6104 6013

Resistance 6145 6147 6184 6195 6204 6205 6296

Good morning. We didn’t quite dip as low as 6120 yesterday but did get a bounce off the 100 Hull MA on the 2 hour chart at 6133 instead, however, there was a real battle with bulls versus bears yesterday and we stayed in quite a narrow range for most of the day. There was a bit of divi hunting buying for the 7 point divi between 16:10 and the closing bell. It was a mixed close in Europe after a bounce in oil prices following a surprise drop in US crude inventories limited losses on the region’s indices. The top of the Bianca channels are 6184 and 6204 for today so there is still a case for shorting the rallies, maybe we wont manage much past 6200 this week.

US & Asia Overnight from Bloomberg

Asian equities fell toward a one-month low after a raft of disappointing company earnings in Japan and the U.S. curbed demand for riskier assets. Australia’s dollar and China’s yuan weakened, while crude oil traded near $46 a barrel.

Consumer-discretionary shares led losses on the MSCI Asia Pacific Index. Toyota Motor Corp. and Bridgestone Corp. were the two biggest drivers of losses on Japan’s Topix index after profit announcements. Australia’s dollar slipped toward a two-month low and China’s yuan weakened for the third time in four days. Crude slipped from a a six-month high, having surged on Wednesday as data showed an unexpected drop in American stockpiles. Copper rose in London, while gold retreated after its biggest gain this month.

With pessimism over the global economic outlook and concern over central banks’ firepower already keeping investors on tenterhooks, the corporate earnings season has provided little in the way of support for equity markets, which lost more than $1 trillion in value last week. U.S. consumer stocks tumbled Wednesday as results from Macy’s Inc. and Walt Disney Co. missed estimates, while Japanese profits have in the main proved disappointing so far.

“There’s just enough out there to keep investors cautious,” said Tim Schroeders, a portfolio manager in Melbourne at Pengana Capital Ltd., which oversees about $1.2 billion in assets. “We’ve got earnings disappointments and currency volatility so people are sitting back and waiting.”

The euro area and India are scheduled to release industrial output data on Thursday, while U.S. weekly jobless claims figures are also due. The Bank of England is seen leaving interest rates unchanged at a monetary policy review, as is Norway’s central bank. European Central Bank Vice President Vitor Constancio will speak in Madrid, and the heads of Federal Reserve Banks for Boston, Kansas City and Cleveland are due to give presentations that may include comments on the U.S. rate outlook. Credit Agricole SA, Nissan Motor Co. and Petroleo Brasileiro SA are among companies reporting earnings.

Stocks

The MSCI Asia Pacific Index lost 0.3 percent as of 1:26 p.m. Tokyo time. Benchmarks in Shanghai and Hong Kong sank to two-month lows and the Topix dropped 0.3 percent. More than 60 percent of Topix members to have reported so far this earnings season announced profits that trailed analysts’ estimates, according to data compiled by Bloomberg.

“Given earnings, we don’t feel comfortable buying Japanese shares,” said Mitsushige Akino, executive officer at Ichiyoshi Asset Management Co. in Tokyo. “Toyota’s results have again confirmed the effect the yen has on corporate earnings.”

Toyota fell as much as 4.5 percent after Japan’s biggest company forecast a 35 percent drop in net income for this fiscal year. Bridgestone sank more than 5 percent after posting a 21 percent slide in first-quarter earnings. CK Hutchison Holdings Ltd. slid to a three-month low in Hong Kong after European Union regulators vetoed the company’s plan to buy U.K. carrier O2 for as much as 10.25 billion pounds ($15 billion).

Futures on the S&P 500 advanced 0.2 percent after the benchmark slid 1 percent on Wednesday. Contracts on the U.K.’s FTSE 100 Index fell 0.3 percent. A Japanese exchange-traded fund tracking Brazilian shares was down 0.7 percent, following a 4.6 percent surge on Wednesday, as the South American country’s Senate votes on whether to force President Dilma Rousseff out of office and into an impeachment trial.

Currencies

Australia’s dollar fell 0.5 percent versus the greenback, leading declines among major currencies. Traders are betting on another interest-rate cut in the next six months after the Reserve Bank of Australia’s unexpected move on May 3. The Aussie’s losses will be limited by investor appetite for higher-yielding AAA-rated assets, keeping the exchange rate in a range, said Takuya Kanda, a senior researcher at Gaitame.com Research Institute Ltd.

The yen weakened 0.2 percent as Bank of Japan Governor Haruhiko Kuroda said risks to the world economy are large and monetary policy can be eased further if needed. The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, rose 0.1 percent after falling 0.4 percent in the last session.

The yuan weakened 0.17 percent in Shanghai, narrowing its premium to the offshore exchange rate after the spread widened on Wednesday to 0.6 percent, the most since February. The divergence prompted speculation this week that the People’s Bank of China would intervene.

“The PBOC will not want to see a very wide onshore-offshore gap, because that will lead to market concerns and capital outflows,” said Gao Qi, a strategist at Scotiabank in Hong Kong. “So if the gap continues to widen, the PBOC will likely take some action to narrow the difference.”

Commodities

West Texas Intermediate crude fell 0.3 percent to $46.10 a barrel after jumping 3.5 percent last session to the highest settlement since Nov. 4. U.S. output declined to 8.8 million barrels a day last week, the lowest level since September 2014, while stockpiles fell 3.41 million barrels, a report showed Wednesday. Analysts surveyed by Bloomberg had projected a 750,000-barrel increase in supplies.

Copper for three-month delivery on the London Metal Exchange gained 0.5 percent, while aluminum added 0.4 percent. Codelco, the world’s biggest copper producer, seesprices rising toward the end of next year as investment cuts hasten a re-balancing of global supply and demand. The LMEX Metals Index, which tracks the six main metals traded on the LME, gained 0.9 percent on Wednesday, rebounding from a one-month low.

Gold fell 0.3 percent, reflecting gains in the dollar. It has surged 20 percent this year as the Fed refrained from raising interest rates and the European Central Bank and Japan stepped up monetary stimulus. A World Gold Council report showed Thursday that global demand in the first quarter was the second-highest on record.

“Investors have increasingly started processing the fact that the world’s central bankers are completely focused on debasing their currencies,” Billionaire hedge fund manager Paul Singer wrote in an April 28 letter to clients.

Bonds

Japan’s 30-year government bonds fell after demand weakened at an auction of the debt. The yield on the securities increased to 0.325 percent from 0.3 percent.

The U.S. also plans to sell debt of that maturity on Thursday, after the notes handed investors a return of more than 10 percent this year. The long bonds yield 2.58 percent — more than any other benchmark maturity in the U.S., the U.K., Germany or Japan — and the securities are rallying as traders push back bets for when the Fed will raise interest rates. Treasuries due in a decade yielded 1.73 percent, little changed from Wednesday. [Bloomberg]

FTSE 100 Outlook and Prediction

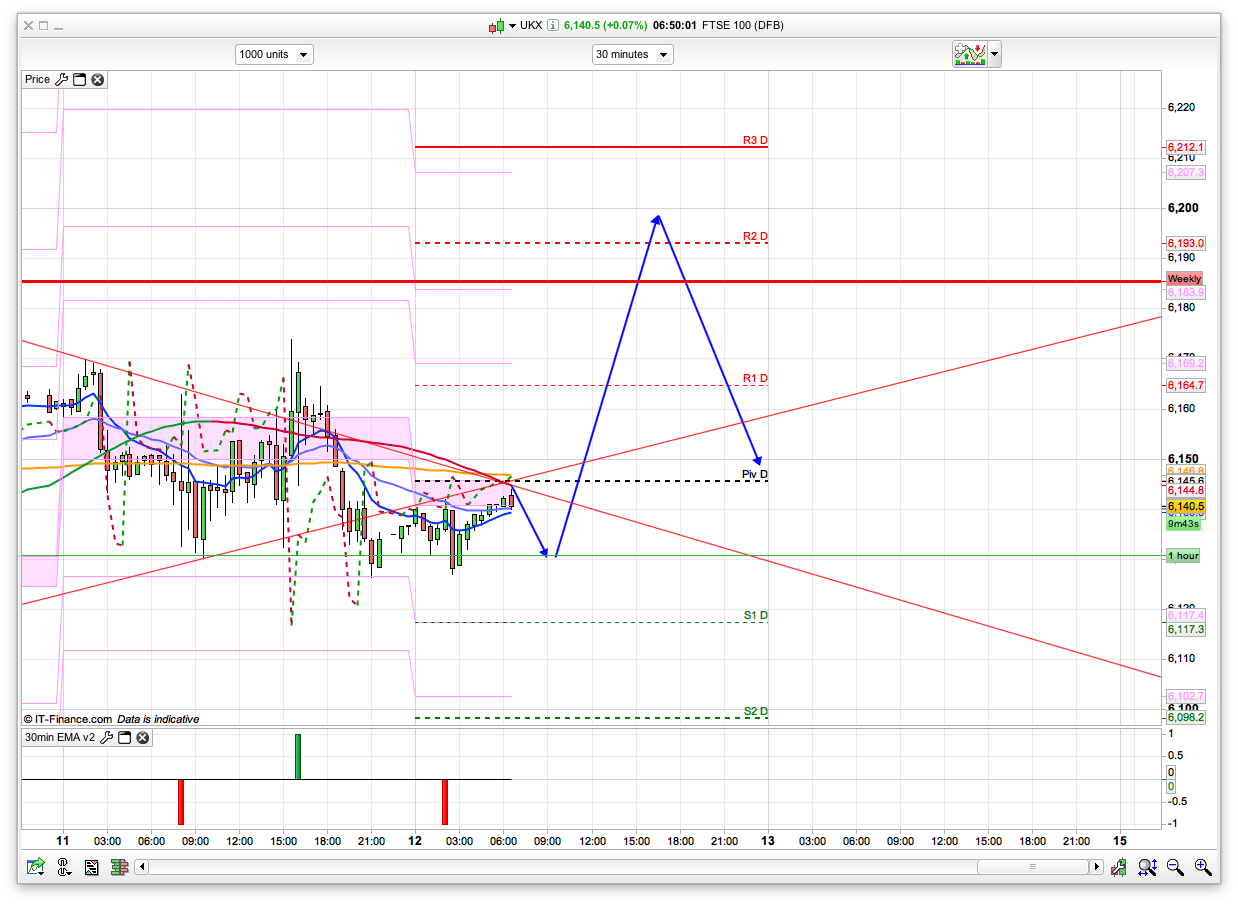

Midday today sees the release of the BoE bank rate figure and the asset purchase target, both expected to remain unchanged at 0.5% and 375bn. We also have inflation report released then, so we may well get some chop around this time. Initially today, and while I am writing this email there is resistance at 6145 where we have the daily pivot and 200ema on the 30min. The 2 hour chart has also gone bearish since that drop from 6180 yesterday afternoon, and is also showing resistance at 6145. The bulls will be keen to break this level initially, but then we have the top of the 2 Bianca daily channels at 6184 and 6204 – so swing shorts around this area are with a go, especially as the 10 day Raff intersecting them at 6195. The coral line has also gone red on the daily now since the drop from 6430, showing a downtrend in place on that time frame. Reading some analysts reports yesterday a few are still expecting a 10% correction in stocks over the next few months, so shorting the rallies would be a good move for the moment. With any luck we will pop higher this morning to trigger those decent shorting areas.