FTSE 100 Support 6802 6796 6790 6786 6770 6750 6711

FTSE 100 Resistance 6832 6834 6844 6850 6864

Good morning. Bit off a funny spike down first thing which didn’t help that early long, however, the 6863 short worked well. The market continued falling for most of the evening ending up around 6820 where it remained overnight. Of course, its all eyes on the US at the moment with the Fed and Jackson Hole meeting, followed by Yellen’s speech tomorrow. U.S. economic data today are forecast to show durable goods orders rebounded in July and services output picked up this month, continuing the run of mixed US data.

US & Asia Overnight from Bloomberg

- Price swings in Asian stocks are the most muted since 2012

- Oil near one-week low after U.S. inventories unexpectedly rise

A dollar rally ran out of steam as most financial markets stabilized ahead of a Friday speech by Federal Reserve Chair Janet Yellen that may shed light on the likely scale and timing of U.S. interest-rate increases. Chinese stocks and iron ore dropped.

The Bloomberg Dollar Spot Index snapped a four-day winning streak that was fueled by hawkish comments from Fed officials.

Fluctuations in the MSCI Asia Pacific Index over the past two weeks have been the most muted since 2012 and gauges of expected price swings in Japanese and Hong Kong equities are near their lows for the year. Crude oil held near a one-week low following an unexpected rise in U.S. stockpiles, while iron ore slid by the most this month.

A rally that drove global equities to their highest level in a year fizzled out since the start of last week amid rising expectations the Fed will raise interest rates in 2016. Monetary tightening in the U.S. risks destabilizing financial markets as central banks in the major economies of Asia and Europe lower borrowing costs and step up stimulus to bolster growth, policies that have led to negative 10-year bond yields in Germany and Japan.

“Everybody is waiting for Yellen, and I’m not sure whether Yellen will provide the impetus all traders are looking for,” said Nicholas Teo, a strategist at KGI Fraser Securities in Singapore. “The Fed rhetoric so far has been balanced although the last two weeks we’ve seen quite hawkish comments.”

U.S. economic data on Thursday are forecast to show durable goods orders rebounded in July and services output picked up this month. Gauges of business sentiment in Germany and U.K. retail sales are also scheduled, while Medtronic Plc and Vivendi SA are among European companies announcing earnings. Brazil’s Senate opens an historic impeachment trial that is expected to result in President Dilma Rousseff’s permanent ouster.

Stocks

The MSCI Asia Pacific Index was little changed as of 1:23 p.m. Tokyo time, with technology stocks advancing and energy companies losing ground. The gauge has moved less than 0.2 percent on each of the last four days.

Benchmarks in Hong Kong, Singapore and South Korea were little changed, while Japan’s Topix index declined 0.2 percent amid trading volumes that were 30 percent below average.

“It’s too scary to buy into Japanese shares” given the possibility markets will be whipsawed following Yellen’s speech, said Mitsushige Akino, a Tokyo-based executive officer at Ichiyoshi Asset Management Co. Shares will be sensitive to the yen, which could surge to 95 per dollar if Yellen indicates a rate increase is off the table, while it will plunge should she suggest a hike is imminent, he said.The Shanghai Composite Index dropped 1.1 percent, set for its biggest loss of the month, on concern the government will act to cool speculative activity in the nation’s financial markets. PetroChina Co. and Cnooc Ltd. fell more than 1 percent in Hong Kong after reporting earnings, while China Construction Bank Ltd. climbed to a 10-month high ahead of its results.

Futures on the S&P 500 Index were steady after the U.S. benchmark dropped 0.5 percent on Wednesday. U.S. stocks could face a significant correction over the next two months as a slew of technical signals suggest the summer rally will lose momentum, according to UBS Group AG.

Currencies

The Bloomberg Dollar Spot Index, which tracks the currency against 10 peers, declined less than 0.1 percent, after climbing 0.8 percent over the last four trading sessions. Fed funds futures indicate a 54 percent chance of a U.S. interest-rate hike this year, up from 36 percent at the start of August. The yen was little changed at 100.48 per dollar and South Korea’s won gained 0.3 percent.

“The market’s just trying to get through the whole event risk” of Yellen’s speech, said Andy Ji, a Singapore-based currency strategist at Commonwealth Bank of Australia. “But after that, what’s driving the market is back to the search for yield and it’s good for emerging markets in general.”

Goldman Sachs Group Inc. sees the pound, the yen and the kiwi as most vulnerable to a potential surprise from Yellen’s speech at the annual monetary-policy symposium in Jackson Hole, Wyoming.

Commodities

West Texas Intermediate crude oil was little changed at $46.75 a barrel. It dropped 2.8 percent in the last session as data showed U.S. inventories unexpectedly rose last week.

Iron ore dropped 3.2 percent in Singapore after Li Xinchuang, a vice chairman at the China Iron & Steel Association, said falling steel production in China should weigh on prices for the raw materials. The price is still up by about 40 percent for the year.

Copper was up 0.4 percent, still near its lowest level in more than two months. Barclays Plc flagged risks of a “sharp slowdown” in demand from China in the second half, after the world’s top user slashed imports to the lowest in 17 months. Inventories tracked by the London Metal Exchange have surged 21 percent over the past three days to the highest since November.

Gold gained less than 0.2 percent, after sliding 2.1 percent over the last four days.

Bonds

U.S. Treasuries due in two years were little changed with their yield at a two-month high of 0.76 percent. The securities are the cheapest they’ve been relative to 30-year notes since the start of 2008 following a run of hawkish comments from Fed officials including Vice Chairman Stanley Fischer and the heads of the New York and San Francisco branches.

“The Fed is likely to hike this year, with December more likely than September,” said Jarrod Kerr, a senior rates strategist at Commonwealth Bank of Australia in Sydney. “There is some room for short-end U.S. yields to push a little higher over 2017.” [Bloomberg]

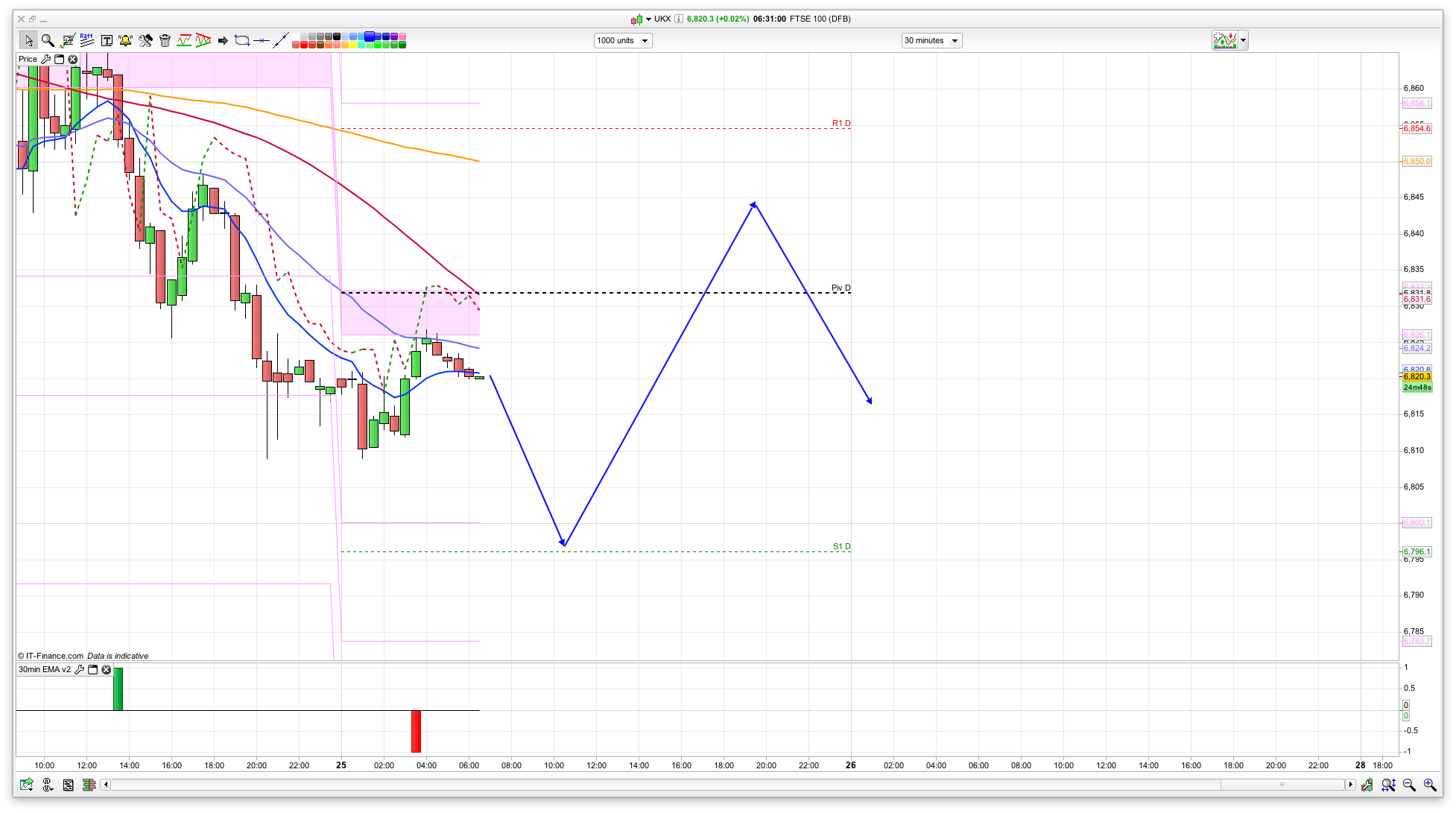

FTSE 100 Outlook and Prediction

Could be an interesting/tricky one today. The 2 hour chart has gone bearish and has resistance from my indicators at 6834 and 6844 so a short around this area is worth a go I feel. I also think we could be on the way to 6750 shortly, especially if the bottom of the Bianca channels break. They are currently at 6790 for the 10 day and 6802 for the 20 day. I have gone for a long from this area on the trade plan in case they hold, however, be prepared to flip to short if they break. We have certainly weakened a little bit since the 6950 level the other day, and yesterdays rally faltered at the 6865 level as expected. The ball is really in the bears court now to make the declines stick, however the bulls will be hoping that the Fed is fairly positive tomorrow. The whole 6800/6810 area is the key one really – it held well the other day but if it keeps getting tested then it will eventually break. Could be a quick trip to 6750 if so.

So fairly simple plan today really but I am favouring the short over the long as a bias – so maybe a larger stake on the short compared to the long. So, yes, could be a tricky one today!