Good morning. Fairly bearish day in the end yesterday, though a bounce on the S&P at the close from the 2100 area I was looking for might be gaining some traction. Will find out today! We are also at the bottom of the 10 day Bianca at 6624 so will be interesting to see if these levels hold.

US & Asia Overnight from Bloomberg

Asian stocks fell, with the regional benchmark index extending its weekly decline, as the commodities rout deepened with oil entering a bear market.

The MSCI Asia Pacific Index fell 0.2 percent to 143.38 as of 9:11 a.m. in Tokyo. The gauge is headed for a 0.9 percent decline this week as global equities traced losses on commodity markets, where concern over supply gluts sent gold to industrial metals and oil tumbling. Adding to commodity investors’ pain is the resurgent dollar, with focus shifting to next week’s Federal Reserve policy meeting amid buoyant economic data. U.S. stocks fell for a third day as earnings results from 3M Co. and Caterpillar Inc. disappointed.

“With the U.S. dollar likely to keep rising as the Fed prepares to raise rates, there’s still some sort of weakness to come in the commodity space,” Angus Gluskie, managing director at White Funds Management Pty in Sydney, who oversees $550 million, said by phone. “The earnings outlook in the U.S. is also somewhat subdued as a result of the strong U.S. dollar. We’re not likely to see a massive rally in the next few months.”

Japan’s Topix index slid 0.2 percent and South Korea’s Kospi index dropped 0.7 percent. Australia’s S&P/ASX 200 Index fell 0.4 percent. New Zealand’s NZX 50 Index slipped 0.1 percent. Markets in China and Hong Kong have yet to open.

The Shanghai Composite Index rose for a sixth day on Thursday, climbing 2.4 percent and sending the benchmark index to its longest stretch of gains since May, as unprecedented government intervention to support equities took root. The Hang Seng China Enterprises Index of mainland shares traded in Hong Kong advanced 0.9 percent.

China Manufacturing

A gauge of Chinese manufacturing due Friday may confirm the sector contracted for a fifth straight month in July.

E-mini futures on the Standard & Poor’s 500 Index gained 0.1 percent. The U.S. equity benchmark index retreated 0.6 percent on Thursday.

The earnings season has been spotty for U.S. companies so far, with sluggish demand overseas damping returns for some multinational companies. Disappointing results from Apple Inc. and Microsoft Corp. earlier in the week sparked a selloff in technology shares. [Ref]

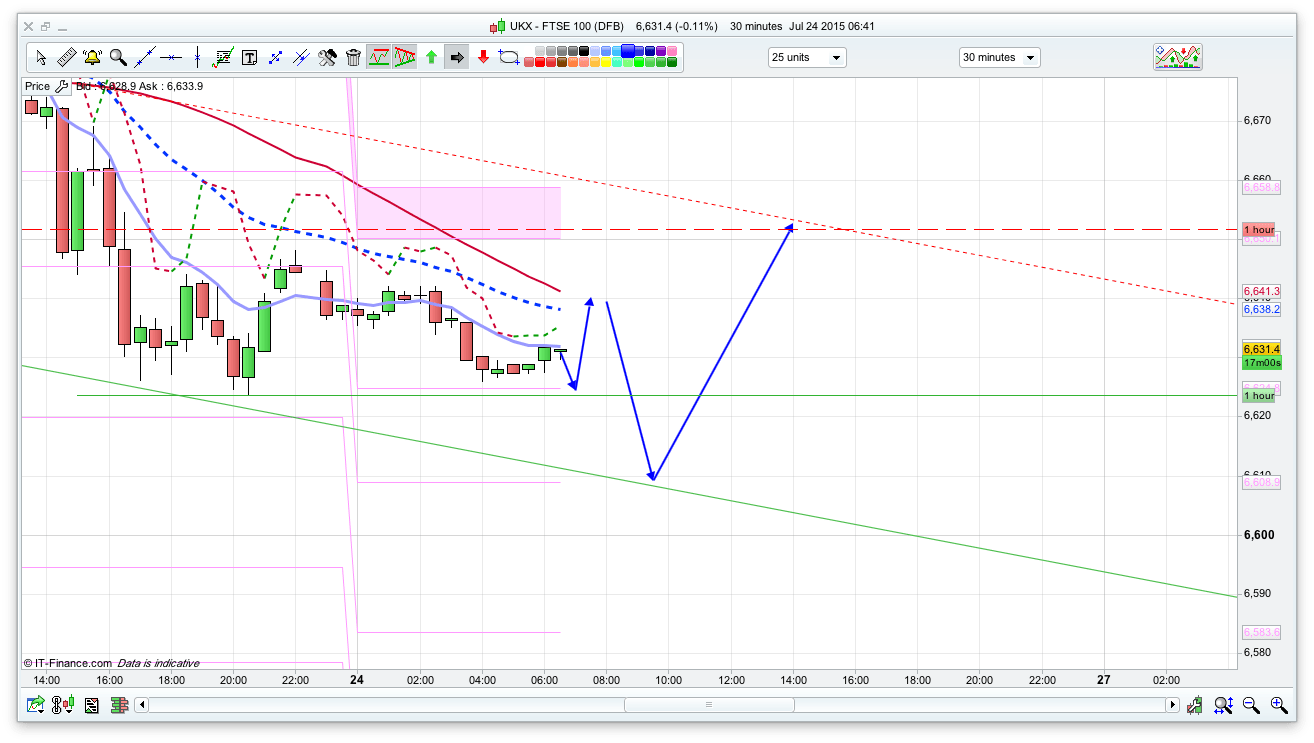

FTSE Outlook

6624 is the bottom of the 10 day Bianca channel and has held so far though there is a decent 30min channel also in play, with support at 6610 (along with a fib level here) and resistance at the 6655 area. The moving averages are bearish to start with and the T3 coral line is also showing resistance at 6640 initially which might scupper any early rises. I have put in a dip to 6610 with the arrows but I do feel about 50% sure that 6624 is going to hold, especially with the S&P bouncing off the 2100 level to 2106 this morning. The bulls will need to break 6634 first thing for 6624 to hold.Generally feeling a bit bullish today, though if 6610 and 2100 on the S&P break then I think we will head down to 6550 and 2090.