Good morning. If you wanted to take a day off to enjoy the warm weather today is a good day to do it. The US is closed for Independence Day and we are going into what could be a lively weekend with a possible Greek referendum, that at the moment is too close to call one way or the other. So much so that IG and other workers have increased their margin requirements substantially for the expected increase in volatility. Would be a good weaken to not hold any position over unless you fancy the risk.

Greece (from Bloomberg)

“People will just wait and see what happens after the referendum,” said Benedict Goette, founder of asset-management firm Compass Capital AG in Zurich. “The dynamics are still difficult for the market. There’s another turn every other day, a new rumor, a new leaked document.”

A measure of expected stock volatility was near a three-year high reached this week. A survey showed more Greeks are going against the government’s call to vote against creditors’ demands. The nation is now living with capital controls and has shut banks and its stock market after its euro-area financial-aid package expired and it missed a payment to the International Monetary Fund. Further bailout negotiations would have to wait until after the referendum.

U.S. Jobs

European equities first remained little changed after the U.S. payrolls report showed employers added 223,000 jobs and the unemployment rate fell to a seven-year low of 5.3 percent. Then, as the dollar weakened against the euro, the Stoxx 600 drifted lower. [Ref]

US & Asia Overnight from Bloomberg

Asian stocks fluctuated, with the regional benchmark gauge set for a weekly decline, as investors awaited Greece’s referendum and weighed U.S. jobs data.

The MSCI Asia Pacific Index added 0.1 percent to 147.08 as of 9:20 a.m. in Tokyo after falling as much as 0.1 percent. The measure is headed for a 0.5 percent decline this week. The monthly U.S labor report indicated job creation advanced in June while pay stagnated and the size of the workforce receded. The Standard & Poor’s 500 Index ended the shortened week down 1.2 percent, the biggest weekly loss since March, after closing little changed Thursday.

“I don’t think the U.S. labor market is getting worse, but it’s not getting better either,” said Nobuhiko Kuramochi, head of investment information at Mizuho Securities Co. “It’s not a reason for the Federal Reserve to hurry into raising interest rates. Polls on the Greek vote show that the results are in the balance. It’s difficult for investors to move.”

Markets across Asia will on Monday be the first to react to the result of Greece’s vote. Prime Minister Alexis Tsipras is calling for a rejection of creditors’ demands, and polls suggest it’s too close to call. Finance Minister Yanis Varoufakis said he’ll quit if voters back austerity.

Two days after Greece missed a payment to the International Monetary Fund, the Washington-based global lender of last resort said the country needs at least a further 36 billion euros ($39.9 billion) from the euro region over the next three years and easier terms to make the debt sustainable.

Jobs Report

U.S. employers added 223,000 jobs in June following a 254,000 increase in the previous month that was less than previously estimated, Labor Department figures showed Thursday. The jobless rate fell to a seven-year low of 5.3 percent as more people left the labor force.

Earnings at private employers held at $24.95 an hour in June on average and rose 2 percent over the past 12 months, matching the mean since the current expansion began six years ago. Wages had increased 2.3 percent in the year ended in May. The participation rate, which indicates the share of working-age people in the labor force, decreased to 62.6 percent, the lowest level since October 1977.

Japan’s Topix index gained 0.1 percent. Australia’s S&P/ASX 200 Index slipped 0.5 percent and New Zealand’s NZX 50 Index added 0.2 percent. South Korea’s Kospi index fell 0.1 percent.

Futures on the Hang Seng Index slipped 0.1 percent and contracts on the Hang Seng China Enterprises Index declined 0.3 percent in most recent trading. Contracts on the FTSE China A50 Index lost 0.7 percent in Singapore, indicating another day of losses in a stock market poised to be the world’s worst performer this week. [Ref]

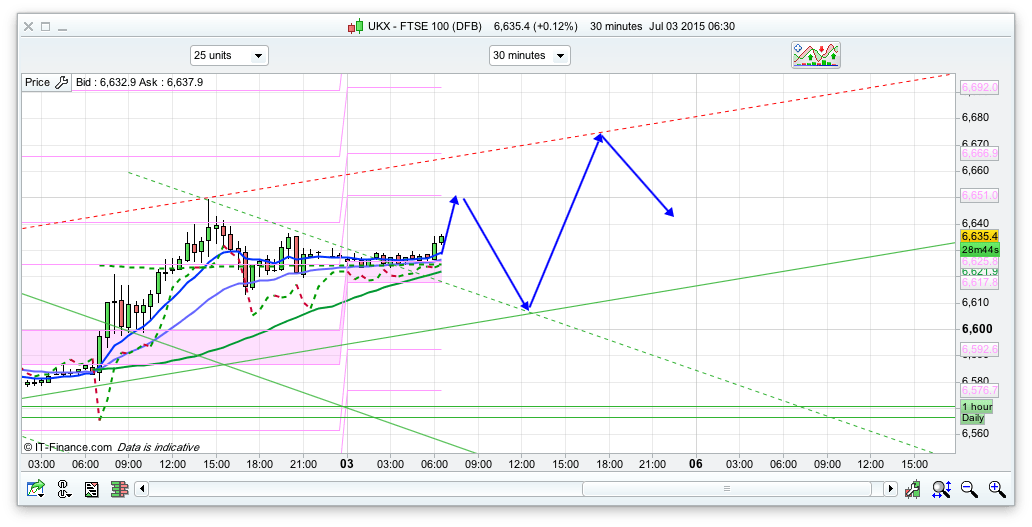

FTSE Outlook

Its a hard one to call today but I have gone for an initial rise to 6650 where we have the top of the 10 day Raff and the first of the fib resistance lines, as well as yesterday high. A dip back towards the pivot at 6618 and possibly even the bottom of that rising 30min channel slightly lower at 6605 before another rise. I am not sure we will see 6728 but if we do then that will be a good shorting area as we have the top of the 10 day Bianca and also the 25ema on daily there. At the moment the polls show the referendum split down the middle so a tough one to call, but then we all know what polls are like! FTSE is cautiously bullish first thing for me again, but will need to see what it does at 6650. A break below that 30min channel will then lead to next support at 6592 then 6548. Might be worth a brave long here as we also have S2 at this level. Pretty much all of today is going to be focussed on the Eurozone and Greece and what may or may not happen. The 30min channel looks a good one to use for trades initially.