Good morning. Nice to have a day without Greece hogging the headlines with will they won’t they stories, making the trades actually work out a lot better. The pivot long took a while to get going but did in the end (at least got a few off that rise) though the 6749 short was a bit lacklustre. Think the markets are relieved that Greece accepted the deal though remains to be seen if the Greek parliament accepts it today.

Greece (from here)

Greek Prime Minister Alexis Tsipras started his pitch for a bailout that’s sparked a revolt in his own party and is struggling to get off the ground as international officials ask new questions about the country’s finances. Tsipras’s comments set up a day of parliamentary maneuvering that threatens to rupture his coalition. Still, opposition lawmakers are likely to back the package at a plenary vote scheduled for about 10 p.m. local time Wednesday.

“We are looking at all the instruments and funds that we could use and all of them seem to have disadvantages or impossibilities or legal objections,” Dutch Finance Minister Jeroen Dijsselbloem, who chairs meetings of his euro-area counterparts, said in Brussels.

Ratification must also be secured in six other parliaments, among them the German lower house, or Bundestag, which will be reconvened on Friday from its summer recess.

For now, attention will focus on Athens as Tsipras tries to steer the measures past his coalition of Syriza and the Independent Greeks. Discussion will begin at committee level at 10 a.m. and then move to a plenary debate at about 2 p.m.

US & Asia Overnight from Bloomberg

China’s stocks fell for a second day after better-than-expected economic data failed to boost investor confidence in the world’s worst-performing equity market and more companies resumed trading.

The benchmark equity index has declined 25 percent over the past month, the biggest loss among 93 gauges globally tracked by Bloomberg, as margin traders unwound bets after a 150 percent rally by the Shanghai Composite over the previous 12 months. Gross domestic product rose 7 percent in the second quarter, government data showed on Wednesday, compared with economist estimates of 6.8 percent in a Bloomberg survey.

“There’s a lack of confidence in the market’s sustainable rally after a big rout,” said Jimmy Zuo, a Shenzhen-based trader at Guosen Securities Co. “There should be a visible improvement in the economy and corporate earnings to bring back solid investor confidence to the market.”

Economic Data

The GDP data was unchanged from the first quarter and was in line with the government’s annual target. Industrial output in June rose 6.8 percent, while fixed-asset investment increased 11.4 percent in the first half, beating estimates, the National Bureau of Statistics data also showed. Retail sales increased 10.6 percent in June, topping a median forecast of 10.2 percent.

“The GDP numbers are really good,” said Bernard Aw, a Singapore-based strategist at IG Asia Pte. “The better-than-expected GDP reading suggested that Beijing may take its foot off the pedal on more stimulus measures for the time being. This will affect sentiment in the stock market.”

Rate Bets

The probability of the Fed raising rates at its September meeting slipped to 27 percent, down from 35 percent on Monday, futures data compiled by Bloomberg showed. For December, the odds of a hike fell to 63 percent from 69 percent. Fed officials in June forecast the central bank would raise borrowing costs twice this year.

FTSE Outlook

So today we are back to all eye on Greece and if they approve and except the most recent bail out offer. The Greek finances really are in a pretty dire state and we have the IMF wanting to stand on the sidelines too. “The dramatic deterioration in debt sustainability points to the need for debt relief on a scale that would need to go well beyond what has been under consideration to date,” said the IMF in a confidential report. The document amounts to a warning that the IMF will not take part in any EMU-led rescue package for Greece unless Germany and the EMU creditor powers finally agree to sweeping debt relief.

I expect we will get a choppy day today as we try and second guess the next twist in the Greek Odyssey. We have had a pretty decent bull run this week so far off the back of the decision Monday morning, to the point where things might be argued to be getting a bit overbought. As such we may have a bit of a pull back today, and a bigger one if the Greek parliament throw out the deal. I imagine they will approve it though as they don’t have a vast array of options!

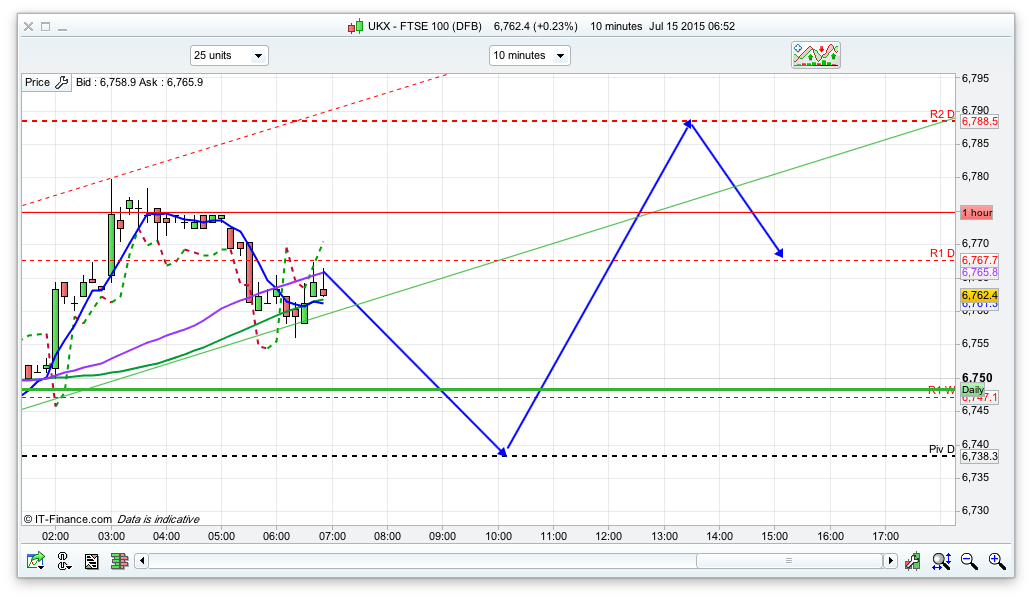

Todays pivot is 6738 and I think we will dip to this level today. As I write the 10min chart is showing a drop from 6765 as a potential trade but probably easier to wait for the moment. So, dip to the pivot then back up to the top of the 20 day Bianca at 6787 I am thinking. We also have some resistance at 6800 – the 200ema and top of the 20 day Raff channel, as well as the declining bearish T3 trend line. Bears might use this as an entry point also. The US is holding onto its recent gains, with the S&P testing 2114 (R1) overnight, with he possibility of 2122 today.