FTSE 100 Support 6852 6835 6820 6803 6797

FTSE 100 Resistance 6866 6869 6888 6903

Good morning. The market held up for most of the day repeatedly testing that 6935 level till Deutsche Bank once again hit the news and sent jitters through the market. Looks like September will end on a bit of a downer now, with resistance at the 6870 area to start with this morning, and more downside likely. The Dax had a torrid day yesterday, dropping over 300 points. The 6928 FTSE short worked well on 2 occasions, and as the morning wore on I didn’t think we would see the 6855 level – but we did and actually saw a bounce from there to 6890 before the bears regrouped. An interesting and once again volatile day!

US & Asia Overnight from Bloomberg

- Deutsche Bank sank to record low in U.S., hitting financials

- Oil near one-month high as most industrial metals retreat

What’s set to be the best quarter for Asian stocks since 2012 is ending on a sour note as concern about the financial health of Germany’s biggest lender unnerves investors, fueling demand for haven assets including the dollar, gold and sovereign bonds.

Financial shares were the biggest contributors to the MSCI Asia Pacific Index’s loss after Deutsche Bank AG slid to a record low in New York, weighed down by a Bloomberg News report that some hedge funds have cut their exposure to the lender. U.S. and U.K. equity index futures fell, while a gauge of the greenback’s strength advanced and the yield on benchmark U.S. Treasuries declined to a three-week low. Gold climbed for the first time in four days and oil retreated from a one-month high. Deutsche Bank’s woes are spooking investors just as the risk of an oil price collapse recedes following an OPEC agreement this week to cut crude output. The bank’s shares have more than halved in value this year amid speculation it will struggle to pay legal bills tied to past misconduct, including a request for $14 billion from the U.S. Department of Justice. The International Monetary Fund said in June that the German lender may be the biggest contributor to systemic risk among the largest financial companies.

“Deutsche certainly weighs on sentiment, and the declines are concerning,” said James Woods, a strategist at Rivkin Securities in Sydney. “Being named the number one bank for global systemic risk, it’s entwined with everyone.”

Stocks

The MSCI Asia Pacific Index dropped 0.9 percent as of 1:48 p.m. Tokyo time, trimming its quarterly advanced to 8.7 percent. Financial stocks accounted for more than a quarter of the decline in the benchmark after U.S.-traded shares of Deutsche Bank tumbled 6.7 percent in the last session.

“Following the report about clients moving to reduce exposure on Deutsche Bank, the possibility of other financial institutions facing similar moves has surfaced,” said Hideyuki Ishiguro, a senior strategist at Daiwa Securities Co. in Tokyo. “Investors, especially foreigners, are moving to cut down on positions in the face of risks arising from European banks.”

Japan’s Topix index and Hong Kong’s Hang Seng Index fell more than 1 percent, leading losses among Asian benchmarks. The latter remains Asia’s best performer of the quarter with a 13 percent advance. The Shanghai Composite Index rose 0.1 percent before financial markets in mainland China shut next week for National Day holidays.

India’s S&P BSE Sensex index fluctuated following a 1.6 percent drop in the last session that marked its biggest loss since June. The nation said Thursday it had attacked terrorist camps in Pakistan, escalating tensions between the two nuclear-armed neighbors. The countries have fought three wars since they split from each other in 1947.

Futures on the S&P 500 slipped 0.3 percent after the underlying index declined 0.9 percent on Thursday. Contracts on the U.K.’s FTSE 100 Index dropped 0.8 percent. Inflation and unemployment data for the euro area are due Friday and the U.S. has consumer spending figures coming.

Currencies

The Bloomberg Dollar Spot Index rose 0.1 percent, after advancing 0.2 percent in the last session. Most emerging-market currencies weakened, led by a 0.5 percent decline in Malaysia’s ringgit.

“The appetite for riskier assets has weakened on worries over euro-zone banks,” said Min Gyeong-won, a currency analyst at NH Futures Co. in Seoul.

Commodities

Crude oil fell 0.7 percent to $47.49 a barrel in New York, after gaining more than 7 percent over the last two days. While Wednesday’s agreement among Organization of Petroleum Exporting Countries imposed an overall production cap on the group of 14 oil producers, it didn’t assign individual limits — that was left to a committee that will report back at OPEC’s next meeting in November.

Most industrial metals retreated, with copper, aluminum and zinc falling by at least 0.4 percent in London. The declines come after the LMEX Metals Index ended the last session at a one-year high. Gold added 0.2 percent.

Bonds

The U.S. 10-year Treasury yield declined two basis points to 1.54 percent as comparable yields on sovereign debt in Australia and New Zealand also dropped to three-week lows.

The rate on Japanese notes due in a decade increased by 1-1/2 basis points to minus 0.075 percent before the central bank announces details of its bond-buying plans for October. The monthly statement, due at 5 p.m. Tokyo time, will provide some insight into where the authority wants yields to be after it last week said monetary policy would be used to shape the yield curve.

The cost of insuring corporate and sovereign bonds against default in the Asia-Pacific region was set to rise for a third straight week, the longest streak of increases since June, according to prices from Australia & New Zealand Banking Group Ltd. and data provider CMA. [Bloomberg]

FTSE 100 Outlook and Prediction

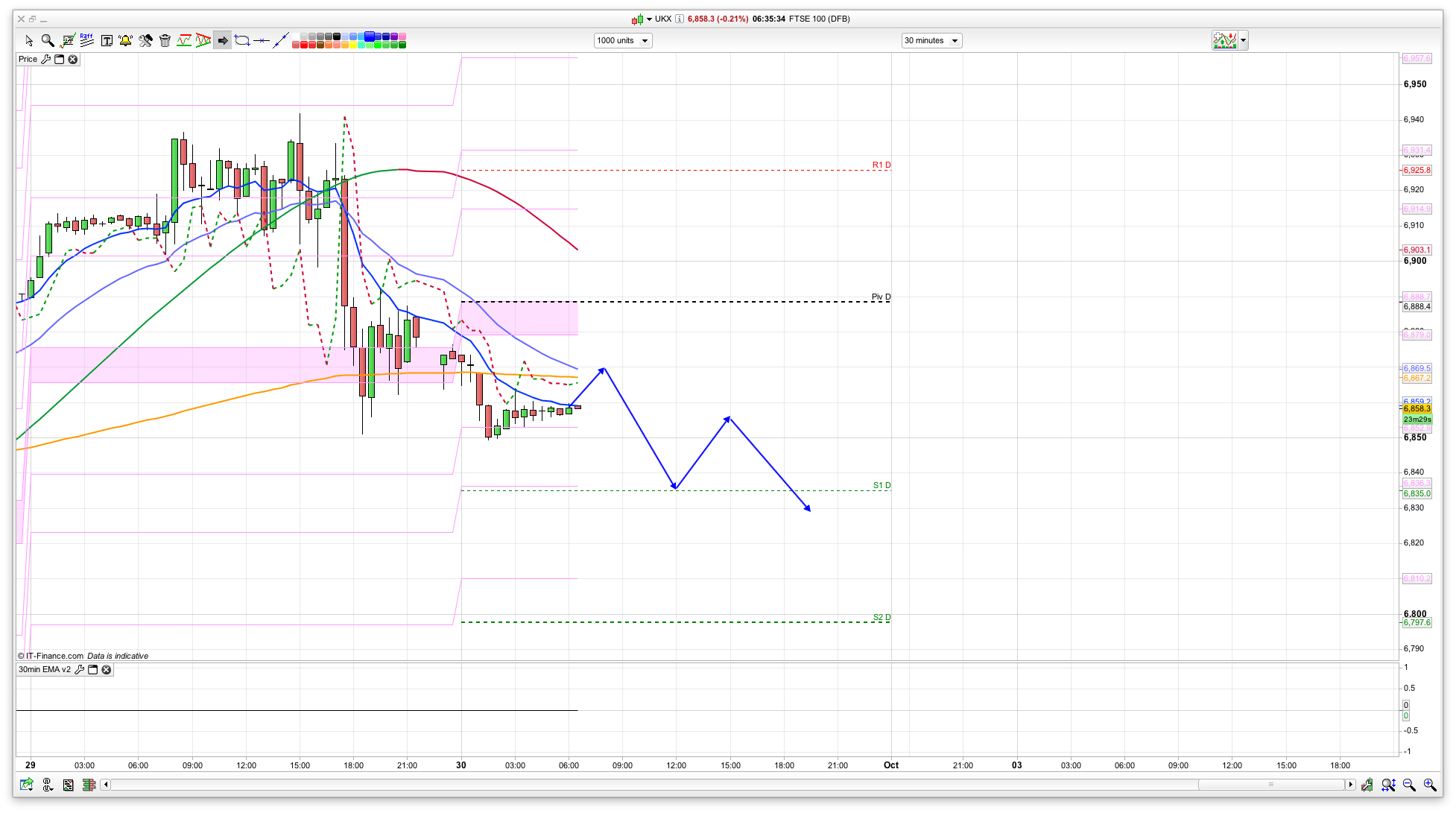

It looks pretty weak to start with, with fairly decent looking resistance at round the 6870 level. We may well see the jitters from yesterday continue, and if the S&P breaks 2144 then we will get a let lower. The bulls had their chance yesterday morning to break the 6938 level and failed so the momentum has swung back to the bears again (volatile isn’t it!). Generally shorting the rallies today is probably the best course of action ahead of the weekend I feel. However, bear in mind that I very much doubt they will allow DB to fail, mainly as they wont want contagion to spread as it will unsettle everything – repeat of 2008 anyone?

Looking at the 30min chart gives short signals at 6869 and 6903 so worth watching both these levels today, though we may struggle to reach the latter, as the 2 hour chart has gone bearish, with resistance at 6866. We are in the middle of the daily Raff and Bianca channels, with the closet channel support being the 10 day Bianca at 6803. Above 6903 then resistance is the 6940 level again, then 6990, then 7030.

Panick over..looks like buyers adding to there positions…

Nice bounce off the fib line down at 6810. Bulls will need to break 6866 now.

I’m having a forex day…. long GBPAUD at 1.7020, looking for 1.7150

i have a sell ticket from 6870, i think we will have a good 50 pip drop to 820.

I’m shorting the dow from 18180

That went well.

you must be screwing, i assume you have been stopped out?

Wish I was screwing mate, it’d be more fun than this. I do like your phone auto-correct, haha! Anyway, no, I’ve got stops at 18280

B*stards

Multiple pints in Birmingham airport, result short heavy at 6880

Still a chance for that lambo then. 🙂

Account gone. I just don’t understand why draw short arrows if they never happen. Just madness.

Keep ya chin up jack. Happens to all, bit like motorcycling. You ain’t a proper rider till you fallen off. Will you reload and keep going?

I will though. B…ds they are today. To break 200EMA like it’s nothing, I’ve never seen it. Shouldn’t have added that much. At the end that rise at 4.09 killed it all. Well, lesson to learn that it happens like this. The main lesson: don’t be greedy and come off with a tiny loss before it’s a big loss.

Maybe good for those who were holding longs and went into minus yesterday.

That’s no surprise today, shorts buying again, buyers are happy…

Think the FTSE will gap down hugely in 20 mins!