FTSE 100 Support 6968 6954 6940 6926 6911 6907

FTSE 100 Resistance 6981 7026 7044 7060

Good morning. Well that surprise GDP figure of 0.5% growth in the 3 months since Brexit caught the bears off guard (and my short) as we rose to 7000 once again. The figure dashed thoughts of a rate cut in the coming months, amid a backdrop of speculation that most major central banks are going to start reining in stimulus measures.

US & Asia Overnight from Bloomberg

A global bonds selloff deepened and Asian stocks held near their lowest level in more than a week amid speculation major central banks are moving closer to reining in stimulus. Commodities advanced amid a retreat in the dollar.

Ten-year sovereign bond yields in the U.S., Australia and New Zealand rose to their highest levels since May, buoyed by expectations that the Federal Reserve will raise interest rates this year. Asian mining stocks rallied with metals and iron ore, though MSCI’s benchmark for regional equities was little changed as investors assessed a mixed bag of corporate earnings. Oil held below $50 a barrel before OPEC talks in Vienna, while a gauge of dollar strength retreated from a seven-month high ahead of an update on U.S. gross domestic product.

Signs of improvement in the global economy are spurring speculation that central banks will abandon ultra-easy monetary policies. The probability of a Fed rate hike this year climbed 5 percentage point this week to 73 percent in the futures market and U.S. GDP growth is forecast to have quickened in the third quarter. The U.K. reported a faster-than-expected expansion on Thursday, virtually killing off bets that the Bank of England will lower borrowing costs in the coming year and Japan’s central bank chief warned that longer-term bond yields may rise.

“We are seeing a shift, with global central banks unlikely to provide additional stimulus and that’s driving bond yields higher and is strengthening the U.S. dollar,” said Niv Dagan, the Melbourne-based executive director at Peak Asset Management LLC. “We’ve had plenty of cautious outlook statements from companies, and investors are adding a bit more defensive exposure in their portfolios and taking some profits off the table.”

The U.S. economy is expected to have expanded at a 2.5 percent annualized pace in the third quarter, an improvement after a tepid nine months of growth, a Bloomberg survey shows. France and Spain will also release GDP updates on Friday and Russia’s central bank has a policy meeting. Euro-area finance ministers meet for talks in Bratislava, Slovakia, and gauges of business and consumer confidence in the region are also scheduled.

Bonds

The yield on 10-year U.S. Treasuries edged up one basis point to 1.86 percent as of 1:54 p.m. Tokyo time, extending this month’s increase to 27 basis points. Rates on similar-maturity bonds in Australia and New Zealand climbed six basis points.

Fixed-income assets are retreating as fund managers boost cash holdings ahead of next month’s U.S. presidential election and as monetary policies show signs of turning less accommodative in the U.S., Europe and Japan. The Bank of Japan shifted to targeting bond levels from its goal to push yields lower, while European Central Bank officials have said said the authority will probably gradually wind down its bond purchases.

“I’m increasing my cash position now,” said Enna Li, who manages a bond portfolio in Taipei for Mirae Asset Global Investments Co., which oversees $93 billion globally. “The U.S. election is a big uncertainty.” Li said she holds 10 percent in cash, versus the usual allocation of 3 percent to 5 percent.

Bonds have lost 2.9 percent in October, according to the Bloomberg Barclays Global Aggregate Index, on course for their worst month since May 2013. Ten-year yields in Germany and the U.K. rose on Thursday to their highest levels since at least June.

Stocks

The MSCI Asia Pacific Index was little changed Friday and down 0.7 percent for the week. A gauge of materials producers gained 0.6 percent and a measure of consumer staples companies was down 0.6 percent. Japan’s Topix index gained 0.5 percent, while benchmarks in Australia, Hong Kong and South Korea declined.

“There are so many risk events coming up, people just sort of want to get those out of the way before they commit,” said James Woods, a strategist at Rivkin Securities in Sydney. “There’s quite a bit of cash sitting on the sidelines, waiting to be deployed.”

Nomura Holdings Inc. jumped more than 5 percent in Tokyo following the release of its earnings, while China Construction Bank Ltd. sank to a two-week low in Hong Kong in the wake of results. Fortescue Metals Group Ltd. advanced more than 3 percent in Sydney, boosted by gains in iron ore prices.

Futures on the S&P/500 Index rose 0.1 percent after the underlying benchmark fell 0.3 percent on Thursday. Amazon.com Inc. slid as much as 9 percent in extended trading after warning it may not make any money in the holiday quarter, while Alphabet Inc. gained after Google’s holding company reported revenue and profit that topped analysts’ estimates.

Currencies

The Bloomberg Dollar Spot Index was down less than 0.1 percent, paring its weekly advance to 0.4 percent. It’s climbed 2.4 percent this month, the best performance since May. The yen advanced for the first time this week.

“The dollar-bullish trend has become clearer and the currency has more leg to go against the yen towards year-end,” said Takuya Kanda, a senior researcher at Gaitame.com Research Institute Ltd.n in Tokyo. “Once uncertainty over the U.S. presidential election is removed, markets will focus on the prospect of a Fed rate hike in December.”

The yuan was little changed near its weakest level in six years amid speculation that China’s policy makers are becoming more tolerant of declines as exports slump and the dollar advances. It’s dropped 1.5 percent in October, set for its biggest monthly loss since an August 2015 devaluation.

Bitcoin surged 8.5 percent this week to $684.23, the biggest increase since June, as yuan declines spurred demand for the cryptocurrency. China accounts for about 90 percent of trading in bitcoins as the digital tender offers its citizens a means to hedge against yuan depreciation amid capital controls.

Commodities

Crude oil rose 0.1 percent to $49.78 a barrel in New York, after rebounding 1.1 percent from a three-week low in the last session. Saudi Arabia and its Gulf nation allies in the Organization of Petroleum Exporting Countries are willing to cut 4 percent from their peak output, Reuters reported Thursday. An OPEC committee meets Friday in Vienna to discuss quotas for members participating in an agreement to cut production, and talks will be held Saturday with producers outside the group, including Russia. Iron ore rallied for a seventh day on the Dalian Commodity Exchange, its longest winning streak since at least 2013. It’s jumped about 10 percent this week, climbing with coal prices amid rising steel output in China.

“Iron ore prices are defying market expectations, due almost exclusively to Chinese steel production continuing to exceed forecasts,” said Gavin Wendt, founding director & senior resource analyst at MineLife Pty in Sydney. “Coking coal prices are also a factor.”

Soybeans in Chicago were headed for a 3.2 percent weekly gain, the best performance in almost four months, after a reported pickup in U.S. exports of the oilseed. [Bloomberg]

FTSE 100 Outlook and Prediction

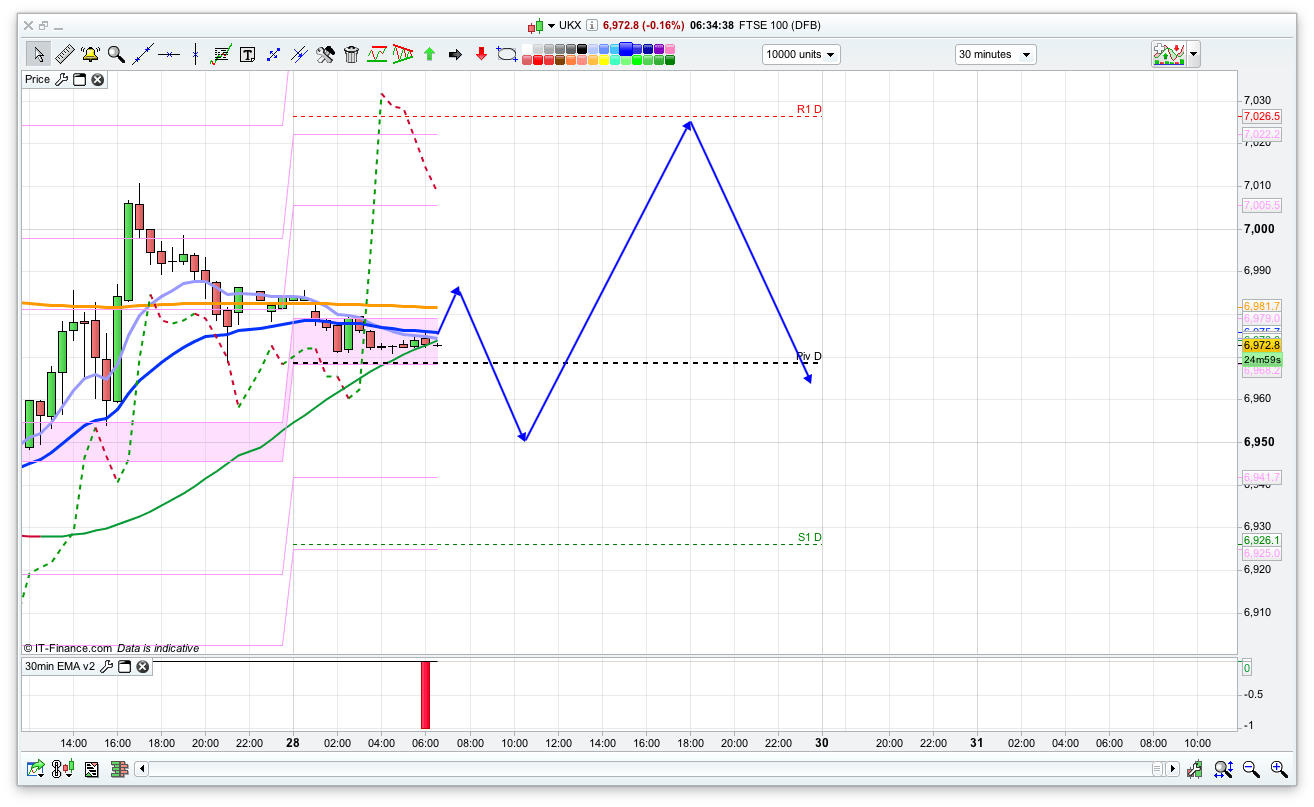

After that rise yesterday from the 6910 level, the 2 hour chart has gone bullish and is showing support at the 6955 level. Worth trying a long here, based purely on that chart. We also have the bottom of the 10 day Bianca channel at 6940 for support, so if the bulls are going to keep yesterdays momentum going then this area should hold as support. If not then back down to 6910. Resistance wise, we have the R1 level at 7026, just above yesterday’s high of 7011, with the 10 day Bianca above that at 7044.

Ahead of the weekend I can see any rally being shorted though so if we do manage to reach 7026, then I think that the bulls from yesterday will be thinking about taking some profit here. So, fairly simple again today, the levels I am watching for trades off today are 6955 and 7026.

morning all.

Very exciting(!) open. indices dropping alongside dollar index.

Got on the down move after the initial pullback and managed to then go long 10 points before the bottom on dax and get 40 points on the way back up. (There was previous support on the H4 around 10590). Feeling very pleased with myself and had 11 winning trades in a row. I should possibly try to turn that into 2 trades – 1 sell and 1 buy, but that’s a test for the days ahead!

GL all, no end of week burnouts!

Busy old morning so far chaps.

Cut through that 2hr support and the bianca like a knife through butter, struggled a dead cat and now bumping along at 30.

I don’t think that 6910 has got much strength either, just a random previous low which could be ignored if we get a roll on, especially next week, if we close the week and the month today below previous daily cash at 47. Will also leave a nice monthly hammer candle for maybe a double top.

Looks awful short term too but I’m not chasing it down, just got a bit left for interest’s sake, stop 48.

I’ll just leave this here (don’t look Si)

http://www.coindesk.com/price/#2016-01-03,2016-10-28,close,bpi,USD

If this rally gets to 60 quickly, a reshort for me.

and a quick -10

Which I scrambled back off the highs.

No idea what to do in the 60’s.

Buy it apparently.

So what happens at 7000, ideas?

God knows tmfp, FTSE has lost the ground – it has no real range. Anyhow I am short now from 7000 and S100 risking profit from last two days!

Yeah I got a medium one going on too, sucker for round numbers, be more convinced if we broke 90/if it was an hour later.

90 will break, I just wanna see 50s again preferably before DOW time 🙂

its going down

BTW US GDP figures are out in 34 mins

Ah ok, tks for that Rick, I think I’ll reduce by half before then

Yeah +20 will do, stop b/e on balance

and +38 on the balance.

I’m knackered, good weekend everyone!

I took +35 on everything.

Have a good weekend tmfp!

FTSE weak today…Dow has just jumped 50 points up…FTSE jumped up 10 points…there is fresh air below 6910

What 30 minutes make..FTSE now strongest lol

Just checked the weekly chart 6900 was the breakout resistance…now it’s support…

ARGH! I slept in – looks like I was very rich at 8.05am! Now I’m not…

Stop rising! Just stop.

Got sucked in by a Gregory Mannarino video last night and went long silver. That’s under water this morning also. A sea of red on my screen… short ftse, long gold, long silver.

My sea of red is beginning to turn blue! Silver and Gold are on the up!

Been shorting these rises all day (and yesterday) however know they are all up I am going to add some big shorts in.

Rate hike, trump, brexit = upside limited. Let the fall begin!

This latest ramp caught me by surprise – managed to go short at the lows on DOW and FTSE seconds beforehand. Damn.

I’d GIVEN UP – BUT WHAT THE HELL IS GOING ON?!!! SEA OF BLUE

Clinton going to PRISON!

Trump rising on the binary. I SAID THIS WAS TOO LOW!!!!

SILVER and GOLD going to the MOON!

I am out tonight!!! Cleaned up! Still some in as the indices are going down to hell !

walked in to the room, wiggled the mouse, saw big drop and shorted… Then instantly regretted it as it bounced off the level I’d sold into. Held my nerve and almost doubled my daily take. yum yum happy weekend everyone…. still think dow should be lower now – sub 18000 style…

Got to say Nick you are good, very good.